Introduction to Behavioral Biases

Behavioral biases refer to the systematic patterns of deviation from norm or rationality in judgment, which often manifest in decision-making processes. These biases emerge from the intrinsic psychological characteristics of individuals and can severely impact the evaluation of risk. In the context of risk decisions, behavioral biases can lead to choices that do not align with objective analysis or statistical realities.

At their core, behavioral biases stem from cognitive limitations and emotional responses that guide individuals’ evaluations. These biases encompass a variety of phenomena, including overconfidence, anchoring, loss aversion, and confirmation bias. Each of these biases can distort an individual’s perception of risk, subsequently affecting their decisions regarding investments, insurance, and other financial ventures.

Overconfidence bias, for instance, is the inclination to overestimate one’s knowledge or predictive abilities, often leading to excessive risk-taking. Individuals may disregard potential downsides, leading them to make uninformed decisions. Anchoring bias occurs when a person relies too heavily on the initial piece of information encountered, which can skew their perception of future risks despite subsequent data that may indicate otherwise.

Loss aversion, a particularly compelling behavioral bias, posits that individuals are more sensitive to losses than to equivalent gains. This phenomenon can lead to overly conservative behaviors, where decision-makers avoid risks even when potential benefits are considerable. Moreover, confirmation bias can prevent individuals from considering alternative information that contradicts their existing beliefs, thereby reducing their ability to make well-rounded risk assessments.

Through understanding and recognizing these biases, individuals can work towards making more rational choices in their risk decisions. By acknowledging the influence of these irrational behaviors, decision-makers are better equipped to confront the complexities associated with risk, thus improving their overall outcomes.

Types of Behavioral Biases

Behavioral biases significantly impact decision-making processes, especially concerning risk in personal finance, investing, and business strategies. Understanding these biases can aid individuals and organizations in making more informed choices. Below are some predominant types of behavioral biases:

Confirmation Bias: This bias occurs when individuals favor information that confirms their pre-existing beliefs while disregarding or undervaluing evidence that contradicts them. For instance, an investor who firmly believes in a stock’s potential may focus solely on positive news articles and ignore negative reports. This selective information gathering can lead to overly optimistic risk assessments and ultimately affect financial decision-making.

Overconfidence Bias: Individuals exhibiting overconfidence bias tend to overestimate their knowledge or predictive capabilities, which can lead to excessive risk-taking in investing. For example, a business leader might overvalue their ability to interpret market trends, resulting in the launch of a new product without conducting thorough market research. This overestimation can produce significant financial losses, especially when market dynamics do not align with the individual’s expectations.

Loss Aversion: Based on the principle that losses are psychologically more impactful than gains, loss aversion can lead individuals to avoid risks in situations where potential advantages exist. A retail investor may hold onto a losing stock, hoping to regain their original investment instead of reallocating those funds to a more promising opportunity. Such behavior underscores how emotional responses can skew rational judgment and impact long-term financial outcomes.

Understanding these biases is crucial for mitigating their effects on risk-related decisions. Recognizing the potential pitfalls of confirmation bias, overconfidence, and loss aversion can empower individuals to engage in more balanced and objective decision-making processes.

The Role of Emotions in Decision-Making

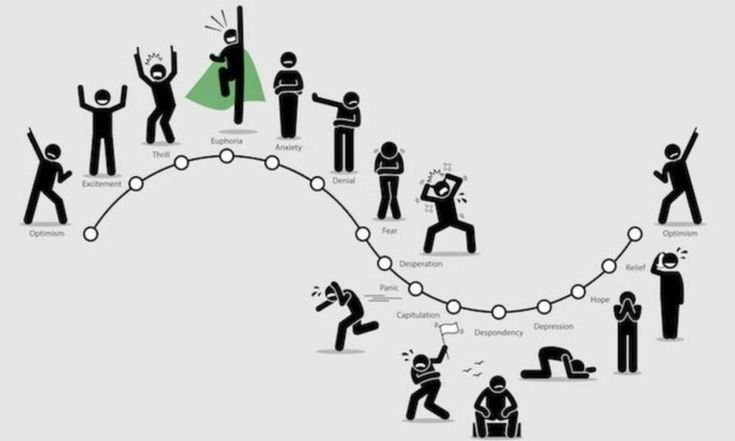

Emotions play a pivotal role in influencing risk-taking behavior during decision-making processes. Among the myriad emotional responses, fear and greed are perhaps the most prominent, significantly impacting the actions individuals take in high-risk scenarios. When faced with uncertain outcomes, emotions can often dictate choices that may deviate from rational or statistically backed decision-making processes.

Fear can lead to risk aversion, causing individuals to avoid potentially beneficial opportunities in favor of a more conservative approach. For instance, investors may shun volatile but potentially high-reward investments purely out of fear of losing capital. This emotional response often clouds judgment and prevents individuals from evaluating risks objectively, thus hindering optimal decision-making.

Conversely, greed can drive individuals to take on disproportionate risks, influenced by the allure of substantial rewards. This phenomenon is observed frequently in financial markets, where traders may engage in speculative behavior, driven by the desire for quick gains. Such emotional impulses can overshadow a rational analysis of the potential downside, leading to poor financial outcomes and increased exposure to risk.

The interplay between fear and greed illustrates a critical aspect of human psychology in risk and decision-making. These emotions can create a cycle of overreaction or inaction, leading to choices that may not align with long-term interests or strategic goals. As a result, individuals are often left to grapple with the consequences of decisions influenced more by emotion than sound reasoning.

Understanding the impact of emotions on decision-making is essential, particularly in high-stakes environments where risks are magnified. Learning to recognize and manage these emotional reactions can significantly improve the quality of decisions made, leading to more favorable outcomes in risk-oriented scenarios.

Cognitive Shortcuts and Heuristics

Heuristics are mental shortcuts that enable individuals to make decisions quickly and efficiently by simplifying complex problems and situations. While these cognitive strategies can be extraordinarily useful in everyday life, they can also lead to systematic errors or biases, particularly in the context of risk assessment. Commonly employed heuristics include the availability heuristic, the representativeness heuristic, and the anchoring heuristic.

The availability heuristic involves evaluating the probability of events based on how easily examples come to mind. For instance, after witnessing a plane crash in the news, an individual may overestimate the risks associated with air travel, neglecting statistical evidence that highlights its safety compared to other modes of transportation. This cognitive shortcut can lead to a distorted perception of risk, influencing decisions and behaviors inappropriately.

Another prevalent heuristic, the representativeness heuristic, leads individuals to judge the likelihood of an event by comparing it to an existing stereotype or typical case. This can result in overlooking significant statistical information, such as base rates, which are essential for accurate risk assessment. For example, when assessing the risk of a disease, one might focus on the profile of a typical patient, ignoring crucial contextual factors that might influence actual probabilities.

The anchoring heuristic occurs when individuals rely heavily on the first piece of information encountered when making decisions. This initial data point can unduly influence subsequent judgments and choices, even if it is irrelevant. In risk scenarios, this may manifest when an initial estimate or figure serves as a baseline, affecting risk perceptions and leading to biased conclusions.

By understanding these cognitive shortcuts and heuristics, individuals and organizations can develop better strategies to mitigate risks and make more informed decisions.

Impact of Social Influences

Social influences play a significant role in shaping individual risk assessments and decision-making processes. Peer pressure, social proof, and herd behavior are prominent social factors that can significantly affect how one evaluates risk. Peer pressure often compels individuals to conform to the expectations or behaviors of their immediate social circles, leading to decisions that may not necessarily align with their personal beliefs or risk tolerance. This influence can be particularly potent in settings where group dynamics are strong, such as in corporate environments or investment groups.

Social proof, the psychological phenomenon where individuals assume the actions of others reflect correct behavior, can also distort risk perception. When faced with uncertainty, individuals may look to the decisions made by others to guide their own. For instance, if a friend or colleague exhibits confidence in a particular investment, others are likely to emulate that behavior without fully assessing the associated risks independently. This can lead to irrational decision-making based on the mere presence of others engaging in similar actions.

Herd behavior further compounds these influences, as individuals may follow the majority in what they perceive to be a shared consensus, often ignoring their judgments. This tendency can lead to market bubbles and crashes, as seen in numerous financial crises throughout history. Understanding these social dynamics is crucial for anyone involved in risk assessment; recognizing the impact of social influences enables individuals to develop a more nuanced understanding of their decision-making processes. Awareness of these biases can foster more critical thinking, allowing for better-informed decisions that prioritize personal risk profiles over conformist tendencies.

Case Studies: Real-Life Examples of Biases in Risk Decisions

Behavioral biases can significantly influence risk decisions, often leading individuals and organizations to make choices that deviate from rational economic behavior. One compelling case study highlighting this phenomenon is the 2008 financial crisis. Financial institutions engaged in excessive risk-taking behavior, largely driven by overconfidence bias. Many executives underestimated the potential risks associated with mortgage-backed securities, believing that property values would continue to rise indefinitely. This overconfidence led to a lack of rigorous risk assessment, contributing to an eventual market collapse that had devastating economic consequences.

Another notable example is the phenomenon of herd behavior observed during the dot-com bubble in the late 1990s. Investors, influenced by the enthusiasm surrounding technology stocks, began to buy shares based solely on market trends, rather than the fundamental value of the companies. This collective behavior, characterized by a disregard for individual analysis, led to inflated stock prices and ultimately a significant market downturn when the bubble burst. The psychological urge to conform to the actions of others illustrated a clear case of social proof bias impacting risk decisions.

A further illustration can be seen in the 2016 U.S. presidential election, where confirmation bias played a crucial role in shaping voter decisions. Many individuals filtered information through the lens of their pre-existing beliefs, resulting in polarized opinions and scant acceptance of alternative viewpoints. This bias not only affected the political landscape but also influenced economic and investment decisions, as uncertainties and speculations around the election outcome impacted market volatility.

These case studies demonstrate that behavioral biases are ubiquitous in risk decision-making processes. By examining real-life instances, it becomes evident how these inherent cognitive distortions can have far-reaching implications, ultimately affecting financial markets and economic stability.

Strategies to Mitigate Biases

Behavioral biases can significantly distort decision-making processes, particularly in high-stakes situations. Therefore, it is crucial to implement effective strategies to recognize and mitigate these biases. One possible approach is the adoption of structured decision-making processes. By employing a systematic framework for decision-making, individuals and organizations can reduce reliance on intuition, which is often influenced by cognitive biases. For example, utilizing methods such as decision trees or cost-benefit analyses can help clarify the potential outcomes and ramifications of each option, facilitating more objective evaluations.

Another effective strategy is awareness training, which seeks to educate individuals about the common behavioral biases that can affect their judgment. Such training can include workshops, seminars, or online courses focused on cognitive psychology and decision-making. By raising awareness of these biases, participants learn to identify them in their thought processes and, in turn, develop mechanisms to counteract their influence. This proactive approach can foster a more reflective and analytical mindset, essential for sound risk decisions.

Incorporating scenario analysis is another valuable technique. This method allows individuals and organizations to explore various potential scenarios and their outcomes. Through this exploration, decision-makers can assess the possible impacts of different choices while gaining insight into how biases may shape their perceptions of risk. Scenarios can be crafted based on real-world data or hypothetical situations, enhancing the decision-making process’s robustness.

Finally, fostering a culture of open dialogue within teams can further mitigate influence from biases. Encouraging diverse viewpoints and constructive criticism enables a more comprehensive view of risks and helps challenge prevailing assumptions. Overall, implementing these strategies can significantly enhance the ability to recognize and mitigate the effects of behavioral biases in decision-making.

Conclusion: Embracing Rational Decision-Making

Understanding behavioral biases is crucial for enhancing our ability to make sound risk decisions. Throughout this discussion, we have highlighted how cognitive biases, such as overconfidence and loss aversion, can distort our perceptions and lead us to make irrational choices that may have adverse consequences. Recognizing these biases is the first step toward mitigating their impact on our decision-making processes.

To foster more rational decision-making, it is essential to adopt strategies that actively counteract these biases. Techniques such as employing decision-making frameworks, seeking diverse perspectives, and utilizing data-driven analysis can significantly improve our judgment when assessing risks. By integrating these strategies, individuals and organizations can cultivate a culture that prioritizes logical analysis over emotional impulses.

Moreover, the promotion of critical thinking skills and continuous learning is imperative in navigating complex risk environments. Encouraging individuals to question assumptions, challenge their own viewpoints, and remain open to new information enhances the potential for informed decision-making. Engaging in regular reflection on past decisions can also serve as an effective learning tool, enabling individuals to identify patterns of bias in their behavior.

Ultimately, embracing rational decision-making is not merely an academic exercise but a necessity in an increasingly uncertain world. By committing to a disciplined approach that recognizes the influence of behavioral biases, we can improve our risk assessments in both personal and professional contexts, leading to more favorable outcomes. As we continue to refine our decision-making abilities, we must remain vigilant against the biases that can compromise our rationality, thereby paving the way for informed and strategic choices.

Further Reading and Resources

For those interested in expanding their understanding of behavioral biases as they relate to risk decisions, a wealth of literature is available. Here, we present a curated selection of books, articles, and research papers that delve deeper into the intricacies of behavioral finance and its impact on decision-making processes.

One foundational book on this topic is “Thinking, Fast and Slow” by Daniel Kahneman. This Pulitzer Prize-winning work explores the dual systems of thinking that drive our choices and the biases that arise from each. Kahneman’s insights into heuristics and cognitive biases lay the groundwork for understanding risk-related decisions.

Another essential read is “Nudge: Improving Decisions About Health, Wealth, and Happiness” by Richard H. Thaler and Cass R. Sunstein. This book discusses how subtle changes in the way choices are presented can significantly influence people’s decisions, offering a practical perspective on behavioral economics and risk management.

For those seeking academic insights, the paper titled “Prospect Theory: An Analysis of Decision under Risk” by Daniel Kahneman and Amos Tversky is highly recommended. It introduces Prospect Theory, which provides a descriptive framework for understanding how people evaluate potential losses and gains, which is critical in risk decision-making.

Additionally, the article “Behavioral Finance: Insights into the Psychology of Investing” published in the Financial Analyst Journal offers a comprehensive overview of the patterns and psychological factors that affect investors’ behavior towards risk. Readers will find this resource invaluable in grasping how emotional and cognitive biases influence financial decisions.

Overall, this collection of readings serves as a starting point for anyone looking to deepen their knowledge of behavioral finance and its implications on risk-related decisions. Engaging with these materials can enhance one’s understanding and application of behavioral insights in various financial contexts.